All Categories

Featured

Table of Contents

If you are a non-spousal recipient, you have the option to place the money you acquired right into an acquired annuity from MassMutual Ascend! Inherited annuities may give a method for you to spread out your tax obligation responsibility, while permitting your inheritance to proceed expanding.

Your choice might have tax or other effects that you might not have thought about. To aid avoid surprises, we advise talking with a tax obligation expert or an economic expert before you decide.

Are Period Certain Annuities death benefits taxable

Annuities don't always comply with the exact same rules as other possessions. Several individuals turn to annuities to capitalize on their tax benefits, along with their distinct ability to assist hedge versus the financial risk of outlasting your money. When an annuity proprietor passes away without ever having annuitized his or her policy to pay routine revenue, the individual named as recipient has some essential decisions to make.

Allow's look extra very closely at just how much you have to pay in taxes on an inherited annuity. For a lot of sorts of residential property, revenue tax obligations on an inheritance are fairly straightforward. The common case includes possessions that are qualified wherefore's called a boost in tax basis to the date-of-death value of the acquired residential property, which efficiently removes any type of integrated resources gains tax obligation responsibility, and offers the successor a tidy slate versus which to gauge future profits or losses.

Immediate Annuities inheritance taxation

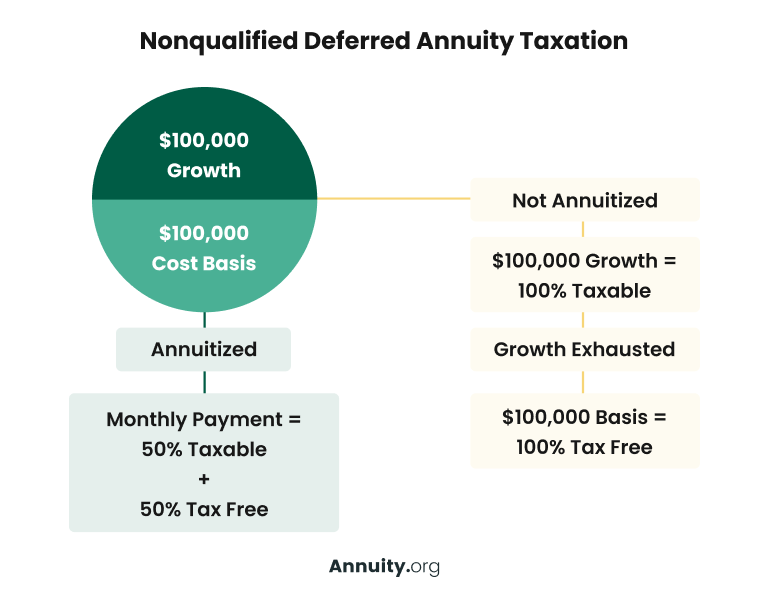

For annuities, the key to taxes is just how much the deceased person paid to purchase the annuity contract, and just how much money the dead individual received from the annuity before death. Internal revenue service Magazine 575 says that, as a whole, those acquiring annuities pay tax obligations similarly that the original annuity proprietor would.

Because case, the tax is much less complex. You'll pay tax obligation on whatever above the expense that the initial annuity owner paid. The quantity that represents the initial costs settlement is treated as tax basis, and as a result excluded from gross income. There is a special exemption for those that are entitled to obtain guaranteed repayments under an annuity contract. Annuity fees.

This turns around the typical regulation, and can be a large benefit for those inheriting an annuity. Acquiring an annuity can be more complicated than getting other home as a beneficiary.

We 'd love to hear your questions, ideas, and point of views on the Expertise Facility in basic or this page specifically. Your input will certainly aid us aid the world spend, better! Email us at. Many thanks-- and Fool on!.

Tax consequences of inheriting a Annuity Income

When an annuity proprietor passes away, the remaining annuity value is paid out to individuals that have been called as beneficiaries.

Nonetheless, if you have a non-qualified annuity, you will not pay earnings taxes on the payments portion of the circulations because they have already been tired; you will only pay income tax obligations on the revenues portion of the distribution. An annuity fatality advantage is a form of settlement made to an individual identified as a beneficiary in an annuity contract, usually paid after the annuitant dies.

The beneficiary can be a child, spouse, parent, and so on. If the annuitant had actually begun getting annuity payments, these settlements and any kind of relevant fees are deducted from the fatality proceeds.

In this instance, the annuity would give an assured survivor benefit to the beneficiary, no matter the staying annuity balance. Annuity survivor benefit are subject to revenue taxes, yet the tax obligations you pay rely on exactly how the annuity was fundedQualified and non-qualified annuities have different tax obligation effects. Certified annuities are funded with pre-tax money, and this indicates the annuity proprietor has actually not paid taxes on the annuity contributions.

Non-qualified annuities are moneyed with after-tax dollars, significances the payments have actually already been strained, and the cash will not be subject to income taxes when dispersed. Any kind of profits on the annuity payments grow tax-deferred, and you will pay income taxes on the earnings part of the distributions.

Tax treatment of inherited Fixed Income Annuities

They can pick to annuitize the contract and receive periodic repayments with time or for the remainder of their life or take a swelling sum payment. Each repayment alternative has various tax obligation effects; a swelling sum settlement has the highest possible tax repercussions since the settlement can press you to a higher earnings tax brace.

, which allows you spread out the acquired annuity settlements over five years; you will pay tax obligations on the distributions you obtain each year. Beneficiaries acquiring an annuity have numerous alternatives to receive annuity payments after the annuity proprietor's death.

This alternative uses the recipient's life span to figure out the dimension of the annuity payments. It provides annuity payments that the beneficiary is qualified to according to their life span. This rule requires beneficiaries to get annuity settlements within five years. They can take numerous settlements over the five-year period or as a single lump-sum repayment, as long as they take the complete withdrawal by the 5th anniversary of the annuity proprietor's death.

Right here are things you can do: As a making it through spouse or a dead annuitant, you can take possession of the annuity and proceed enjoying the tax-deferred standing of an acquired annuity. This allows you to avoid paying taxes if you maintain the cash in the annuity, and you will just owe revenue taxes if you get annuity settlements.

You can trade a qualified annuity for an additional certified annuity with much better functions. You can not exchange a certified annuity for a non-qualified annuity. This advantage is a reward that will certainly be paid to your recipients when they inherit the staying equilibrium in your annuity.

{kind=link}

Table of Contents

Latest Posts

Highlighting Fixed Indexed Annuity Vs Market-variable Annuity A Closer Look at How Retirement Planning Works Defining Variable Vs Fixed Annuities Pros and Cons of Fixed Vs Variable Annuity Pros And Co

Exploring Variable Annuity Vs Fixed Annuity Key Insights on Your Financial Future Defining the Right Financial Strategy Features of Annuity Fixed Vs Variable Why Variable Annuities Vs Fixed Annuities

Analyzing Strategic Retirement Planning Key Insights on Your Financial Future What Is Choosing Between Fixed Annuity And Variable Annuity? Pros and Cons of Various Financial Options Why Choosing the R

More

Latest Posts